USPS Thrift Savings Plan (TSP): Your Complete Guide to Building a Secure Retirement

Most USPS employees know TSP exists but far fewer understand just how much wealth it can quietly build over a career. Having spent time helping postal workers navigate their federal benefits, I’ve seen firsthand how a simple contribution decision made early can mean the difference between a comfortable retirement and a stressful one.

This guide covers everything from enrollment and fund selection to loans, withdrawals, and smart maximization strategies. Whether you just got hired or you’re counting down your final years in uniform, there’s something here that can improve your retirement outlook today.

What Is the USPS Thrift Savings Plan (TSP)?

Think of TSP as your personal retirement engine one that runs on smart contributions and investment choices, and one that only you control. Administered by the Federal Retirement Thrift Investment Board (FRTIB), the Thrift Savings Plan is a tax-advantaged, defined-contribution retirement savings plan available to all federal government employees, including every USPS worker across the country.

For USPS employees under FERS the Federal Employees Retirement System retirement income rests on three pillars:

- FERS Basic Benefit: a traditional pension calculated from your years of service and salary

- Social Security: you pay into it throughout your career and collect benefits at retirement

- Thrift Savings Plan (TSP): your personal investment and savings account

What makes TSP stand out from the other two is simple: it’s the only pillar you actively control. Your pension and Social Security are largely fixed. TSP, on the other hand, can grow aggressively based on how much you contribute and which investment choices you make. That flexibility is exactly what makes it so powerful—and exactly why it’s worth taking the time to understand it fully. Whether you’re exploring new features or managing your work benefits, USPS LiteBlue Benefits can help you make the most of everything the platform offers.

How Does the USPS TSP Work?

At its core, TSP works like a private-sector 401(k) plan money comes out of your paycheck, goes into your account, and grows over time through investment. But the details matter, especially when it comes to how and when you pay taxes.

You have two contribution options:

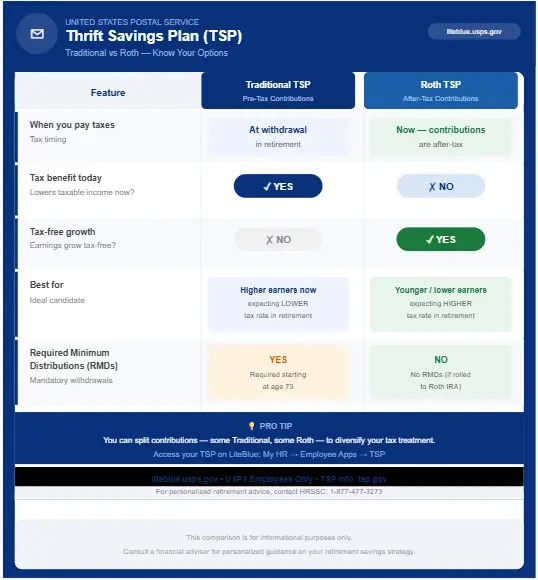

- Traditional TSP: contributions are made pre-tax, which lowers your taxable income today. You pay taxes when you withdraw funds during retirement.

- Roth TSP: contributions are made after-tax, so there’s no immediate tax break. But your money grows tax-free, and qualified withdrawals in retirement are completely tax-free.

You can split contributions between both Traditional and Roth TSP in the same year as long as your combined contributions don’t exceed the IRS annual limit.

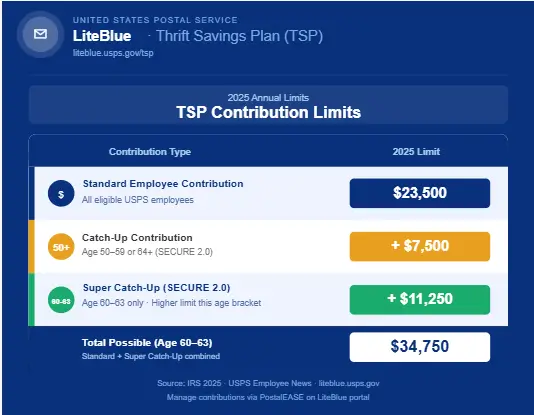

2025 Contribution Limits

One important note: the USPS employer match does NOT count toward your personal contribution limit. That’s free money sitting on top of whatever you put in.

USPS Employer Contributions The Free Money You Cannot Afford to Miss

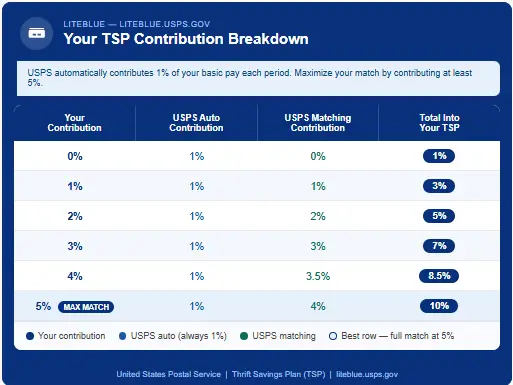

This is the part that genuinely surprises most new postal employees and honestly, it should be talked about far more than it is. USPS contributes to your TSP account on your behalf, and part of that contribution happens whether or not you put in a single dollar yourself.

Here’s exactly how the matching works for FERS employees:

Contribute just 5% of your basic pay, and USPS adds another 5% on top a 1% automatic contribution plus a 4% match. That’s 10% of your basic pay flowing into your retirement account every period, but you only paid half of it. In my experience, no pay raise at USPS will ever beat that kind of return.

Vesting Schedule for Agency Contributions

- The 1% automatic contribution vests after 3 years of federal service (2 years for certain positions)

- Matching contributions vest immediately

- CSRS employees under the Civil Service Retirement System do not receive agency matching contributions but you can still contribute your own money to TSP and benefit from tax-advantaged growth

Who Is Eligible for USPS TSP?

The short answer: nearly everyone. All USPS career employees are eligible to participate in TSP with no waiting period to begin contributing.

| Employee Type | TSP Eligibility |

|---|---|

| Career USPS employees (FERS) | Fully eligible, including agency match |

| Career USPS employees (CSRS) | Eligible to contribute; no agency match |

| Non-career / PSE / CCA employees | May contribute; limited or no agency contributions |

Automatic Enrollment

If you were hired on or after July 31, 2010, you were automatically enrolled in TSP at a 3% default contribution rate into Traditional TSP. That money comes out of your paycheck without you doing anything.

But here’s the problem 3% is not enough. The default rate does not capture the full employer match. To get the maximum free money from USPS, you need to contribute at least 5%. Leaving it at 3% means you’re handing back part of your compensation every single pay period.

How to Enroll in or Modify Your USPS TSP

There’s no open enrollment window for TSP you can start, stop, or change your contributions at any time of the year. Here are your three options:

Method 1: LiteBlue PostalEASE (Online Recommended)

- Go to liteblue.usps.gov and log in with your Employee ID and PIN

- Navigate to PostalEASE under “Employee Apps – Quick Links”

- Select Thrift Savings Plan from the menu

- Enter your desired contribution percentage Traditional TSP, Roth TSP, or a split between both

- Confirm and save your changes

- Changes typically take effect within 1–2 pay periods

Method 2: PostalEASE by Phone

- Call 1-877-477-3273

- Select Option 1 for PostalEASE

- Follow the automated prompts to enroll or update your contribution

Method 3: Employee Self-Service Kiosk

Many USPS facilities have Employee Self-Service Kiosks where you can access PostalEASE directly and modify your TSP contribution on the spot no computer or phone needed.

Understanding TSP Investment Funds

Once your money is in TSP, you decide where it goes. TSP offers two broad categories of funds, and your choice here has a massive impact on long-term growth.

Lifecycle (L) Funds Best for “Set It and Forget It”

Lifecycle funds automatically adjust their investment mix as you approach your target retirement date shifting from aggressive stocks toward conservative bonds over time to protect your savings.

| Fund | Target Retirement | Asset Mix |

|---|---|---|

| L Income | Already retired / near retirement | Very conservative |

| L 2025 | Retiring around 2025 | Conservative |

| L 2030 | Retiring around 2030 | Moderately conservative |

| L 2035–2065 | Retiring in future decades | Progressively more aggressive |

If you don’t want to actively manage your investments, simply pick the L Fund closest to your expected retirement year and let it do the work.

Individual Funds For Active Investors

| Fund | What It Invests In | Risk Level |

|---|---|---|

| G Fund | U.S. Government securities | Very Low |

| F Fund | U.S. bond market index | Low |

| C Fund | S&P 500 index (large U.S. companies) | Medium-High |

| S Fund | Small and mid-size U.S. companies | High |

| I Fund | International stocks | High |

A general age-based approach works well here:

- Younger employees (20s–40s): Lean heavier toward C, S, and I funds for long-term growth

- Mid-career employees (40s–50s): Begin balancing with G and F funds to reduce risk

- Near retirement (5–10 years out): Shift significantly toward G and F funds to protect your savings

You can change your contribution allocation and make interfund transfers anytime at tsp.gov.

Traditional TSP vs. Roth TSP Which Should You Choose?

The decision really comes down to one question: are you in a higher tax bracket now, or do you expect to be in retirement?

A common and effective strategy is to contribute enough to Traditional TSP to reduce your taxable income to a comfortable bracket, then direct any additional contributions into Roth TSP for long-term tax-free growth. You get the best of both worlds.

TSP Catch-Up Contributions For Employees Age 50 and Older

Once you hit 50, the IRS gives you permission to accelerate your savings beyond the standard limit and you should absolutely take advantage of it.

- Age 50–59 or 64+: Extra $7,500 per year above the standard limit

- Age 60–63 (SECURE 2.0 Super Catch-Up, effective 2025): Extra $11,250 per year

These additional contributions can go into Traditional TSP, Roth TSP, or split between both. You don’t need to file a separate form just set your contribution amount above the standard limit through PostalEASE and TSP automatically applies the catch-up rules.

The years between your 50s and retirement are your highest-earning, highest-saving window. This is the time to push hard and fill every gap in your retirement account.

TSP Loans Borrowing from Your Own Retirement

TSP allows you to borrow from your own account balance in two situations:

General Purpose Loan

- Can be used for any reason

- Repayment term: 1–5 years

- No documentation required

Residential Loan

- Must be used to purchase or build a primary residence

- Repayment term: 1–15 years

- Documentation of the real estate transaction is required

Loan limits sit between $1,000 and the lesser of $50,000 or 50% of your vested account balance.

One caution worth taking seriously: TSP loans don’t trigger taxes or penalties since you’re paying yourself back but the borrowed money stops growing in the market during that time. If you miss payments, the loan can be declared a taxable distribution, which creates a tax bill you weren’t planning for.

TSP Withdrawals Accessing Your Money in Retirement

In-Service Withdrawals (While Still Employed)

- Age-based withdrawal: Once you reach age 59½, you can make penalty-free withdrawals from TSP while still working

- Financial hardship withdrawal: Available in genuine hardship situations, but subject to taxes and a 10% early withdrawal penalty

Separation from Service (Retirement or Resignation)

Once you leave USPS, you have several options for your TSP balance:

- Leave the money in TSP and continue benefiting from ultra-low administrative fees

- Withdraw in a lump sum taxable in the year you receive it

- Set up monthly payments based on a fixed dollar amount or life expectancy

- Purchase a TSP annuity for guaranteed income for life

- Roll over to a Traditional or Roth IRA, or another employer’s plan, for more investment options

Required Minimum Distributions (RMDs)

Starting at age 73, the IRS requires minimum distributions from your Traditional TSP each year. Roth TSP balances are also subject to RMDs unless you roll them into a Roth IRA before that point.

Portability What Happens to Your TSP If You Leave USPS?

Your TSP account belongs to you not USPS. Whether you retire, resign, or transfer to another federal agency, your savings go with you. Your options are:

- Keep it in TSP: recommended for most people, given TSP’s annual administrative fee of just 0.048%, which is far lower than most retail mutual funds or private 401(k) plans

- Roll it into a new employer’s 401(k)

- Roll it into a Traditional or Roth IRA

That 0.048% fee is not a typo it’s one of the lowest expense ratios of any retirement plan in the country. Even after leaving postal service, keeping your balance in TSP often makes strong financial sense.

Smart Strategies to Maximize Your TSP

Getting TSP right isn’t complicated but it does require intentional decisions at each stage of your career.

- Always contribute at least 5% — this is non-negotiable. Anything less leaves USPS matching money on the table every single pay period.

- Increase contributions after every pay raise — each time you receive a step increase or promotion, bump your TSP contribution by at least 1%. The compound growth over decades makes even small increases significant.

- Take full advantage of catch-up contributions in your 50s and 60s — the window between age 50 and retirement is your highest-earning, highest-saving opportunity.

- Review your fund allocation every year — your age, risk tolerance, and retirement timeline change over time. Your investment strategy should too.

- Use the TSP Retirement Income Calculator at tsp.gov — free tools let you project account balance growth based on your current contribution rate, investment returns, and expected retirement date.

- Coordinate TSP with your FERS pension and Social Security — use LiteBlue eRetire or a financial planner to understand how all three income streams combine into a realistic monthly retirement income.

Key TSP Resources for USPS Employees

| Resource | How to Access |

|---|---|

| TSP account management | tsp.gov |

| Enroll or change contributions | liteblue.usps.gov → PostalEASE |

| Phone enrollment / changes | 1-877-477-3273, Option 1 |

| TSP ThriftLine (automated account info) | 1-877-968-3778 |

| Retirement planning tools | LiteBlue → eRetire |

| TSP educational publications | tsp.gov/publications |

FAQs about USPS Thrift Savings Plan (TSP)

LiteBlue Benefits Overview

Conclusion

The USPS Thrift Savings Plan is not just a retirement account it’s one of the most valuable financial tools available to any American worker, public or private. Between the employer match, tax advantages, ultra-low fees, and flexible investment options across G, F, C, S, and I funds, TSP gives every postal employee a genuine, achievable path toward financial security in retirement.

The hardest part isn’t understanding how it works it’s getting started and staying consistent. Contribute at least 5% from day one. Increase that percentage with every step increase or promotion. Review your fund allocation every year as your retirement timeline shortens. And if you’re 50 or older, treat the Super Catch-Up contribution limit as a target, not a ceiling.